8–10

Auditors across roles, seniority levels, and three countries involved throughout the process

Audit management & planning platform

Auditing large and complex organizations is a multi-phase process governed by ISA standards, but those standards define what must be done, not how. In practice, audit firms fill that gap with a patchwork of tools: Excel workbooks, proprietary templates, and specialized software, each covering a different slice of the process. Auditors piece their work together across these disconnected systems with no shared structure and no single source of truth. At a firm the size of Cedra, where auditors operate at different seniority levels, carry different responsibilities, and each have their own preferred ways of working, that fragmentation compounds. Every team, every office, every auditor follows their own approach.

Cedra set out to change that by building a unified auditing platform: one tool where auditors of every role and level of seniority can carry out the full audit lifecycle, from understanding the client entity and assessing risk, through planning and executing procedures, to internal review, sign-off, and closure. The platform needed to bring structure and consistency to a firm where none existed, while remaining flexible enough to support audits of varying scale and complexity. This project covers the UX design of that platform, across its most foundational and complex modules.

Designing a unified platform for a fragmented, multi-role audit environment surfaced challenges that went beyond the interface:

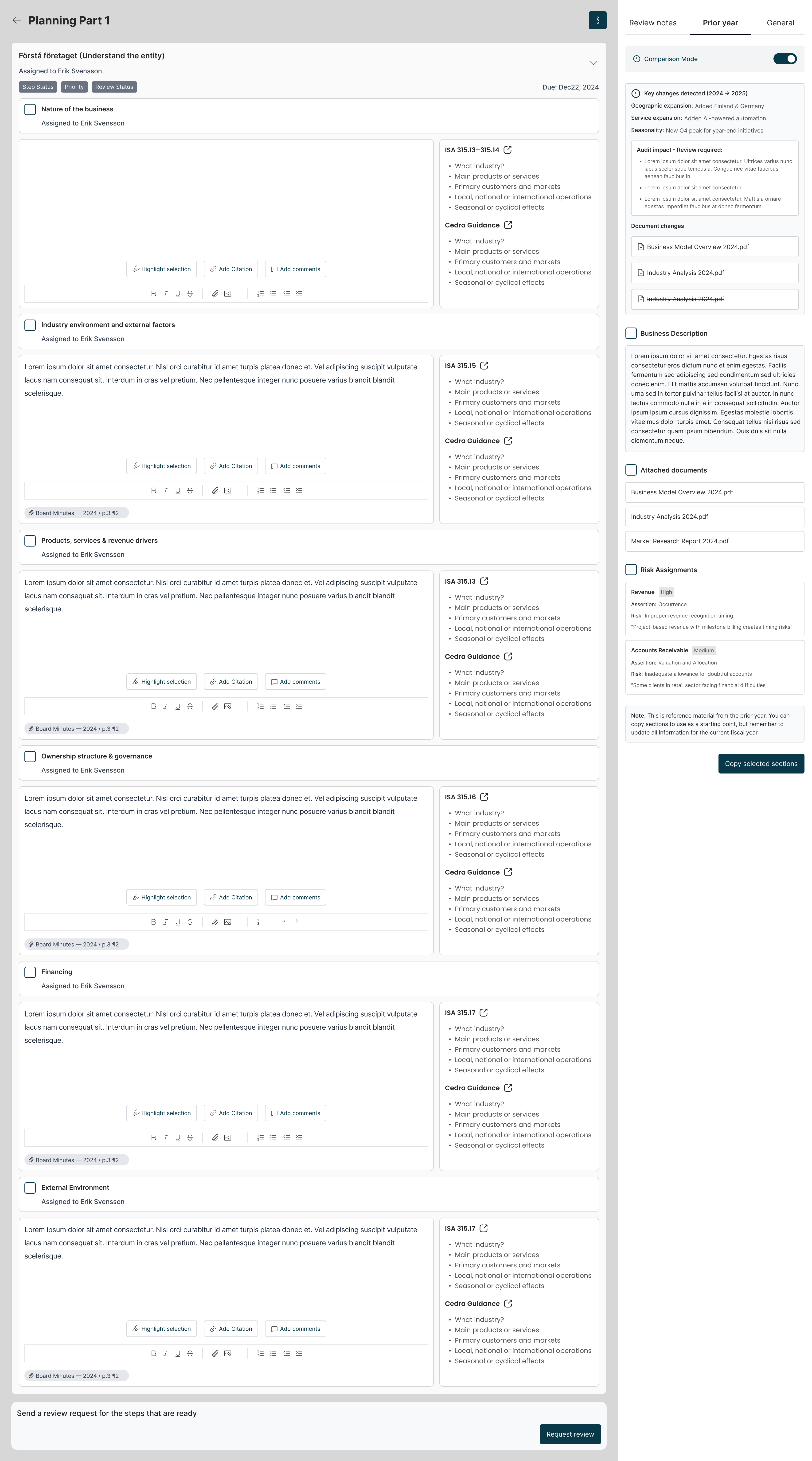

The platform covers the full audit lifecycle in a single tool. Auditors begin with ISA 315, documenting their understanding of the client entity: the business model, internal controls, fraud considerations, and key processes. As they work through this phase, any identified risks can be assessed directly in context. When they move into the formal risk assessment and planning phase, those risks are pre-populated, already connected to the relevant financial statement lines and their related assertions. From there, auditors define the procedures that respond to each risk, assign ownership, set timelines, and can request any missing documentation directly from the client, all within the same environment.

The result is a fully traceable chain: from business understanding through risk, to procedures, to execution. Nothing lives in a spreadsheet, nothing is carried across manually.

End-to-end audit workflow — from entity understanding through to final reporting, all within a single connected platform.

Three distinct roles interact with the platform. Each role enters a tailored default view that surfaces exactly what they need to act on, without requiring them to navigate to it.

Early wireframe from the risk assessment flow, used in section-level testing sessions with the auditor working group.

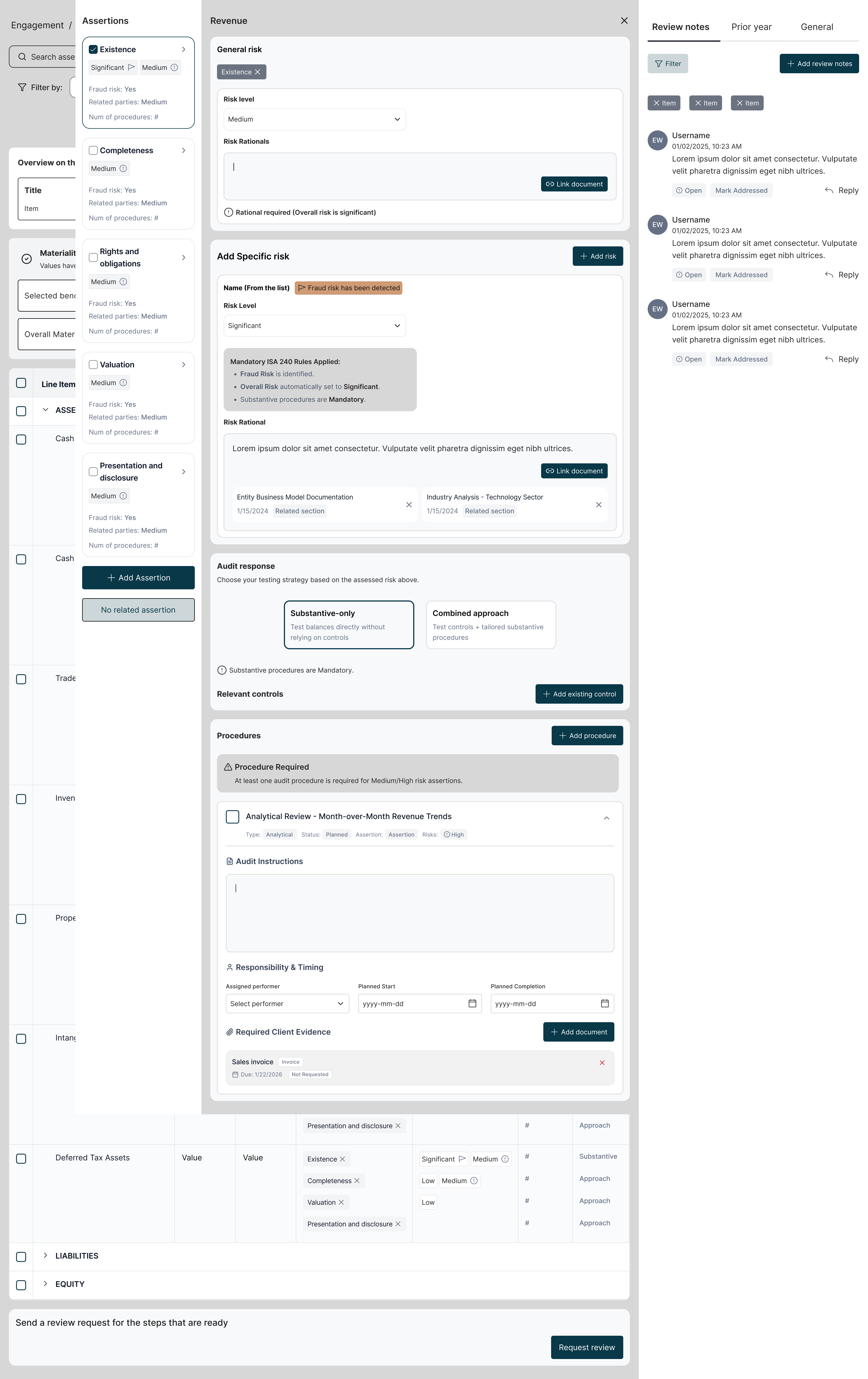

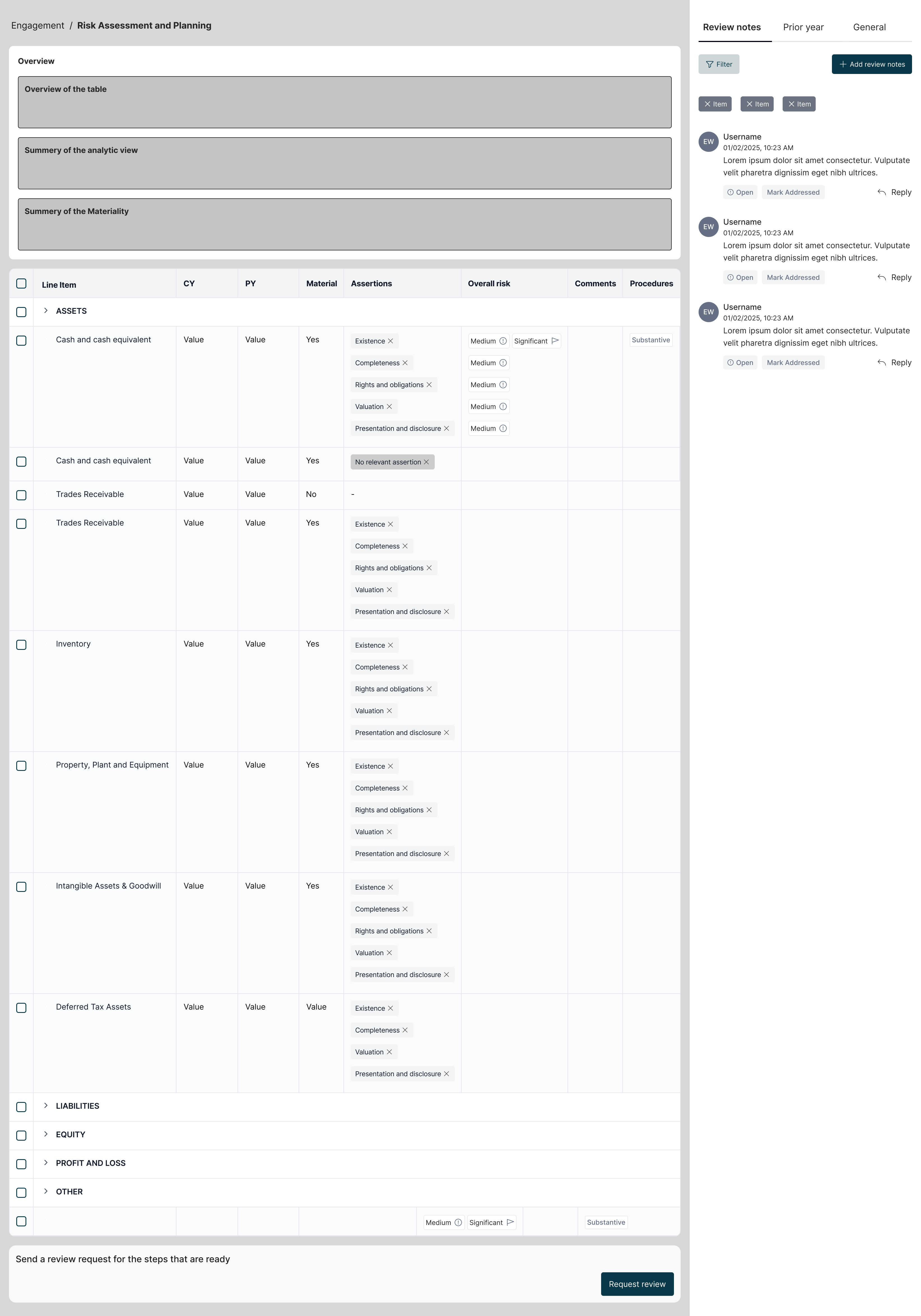

The most complex design challenge was risk assessment and planning. The data was inherently layered: financial statement lines sit at the top, each carrying associated risks, each risk requiring an audit response and one or more procedures. Auditors needed to navigate between lines, see current and prior year values side by side, assess risk in context, and define procedures, all without losing sight of the overall picture. They also needed access to the materiality assessment from within this flow, because materiality thresholds directly inform which risks matter.

The structural answer was a financial statement overview as the anchor: all FS lines visible at once with their current and prior year values. From there, auditors drill into any line to assess risk, document their rationale, select their audit response, and define procedures, either from a library, from prior year, or custom. Every action stays connected to the line that triggered it, so the audit record remains traceable throughout.

The role dimension added another layer. A performer arriving in the system wanted their task queue. A signing auditor wanted to see what awaited their signature. A reviewing auditor wanted to see what needed their review. The solution was role-aware entry points into the same connected data, not separate flows, but different default views of a single audit record.

The traceability chain — every procedure is connected back to the assertion, FS line, and risk that justified it.

Entity understanding interface — auditors document business context, internal controls, and flag risks directly in context.

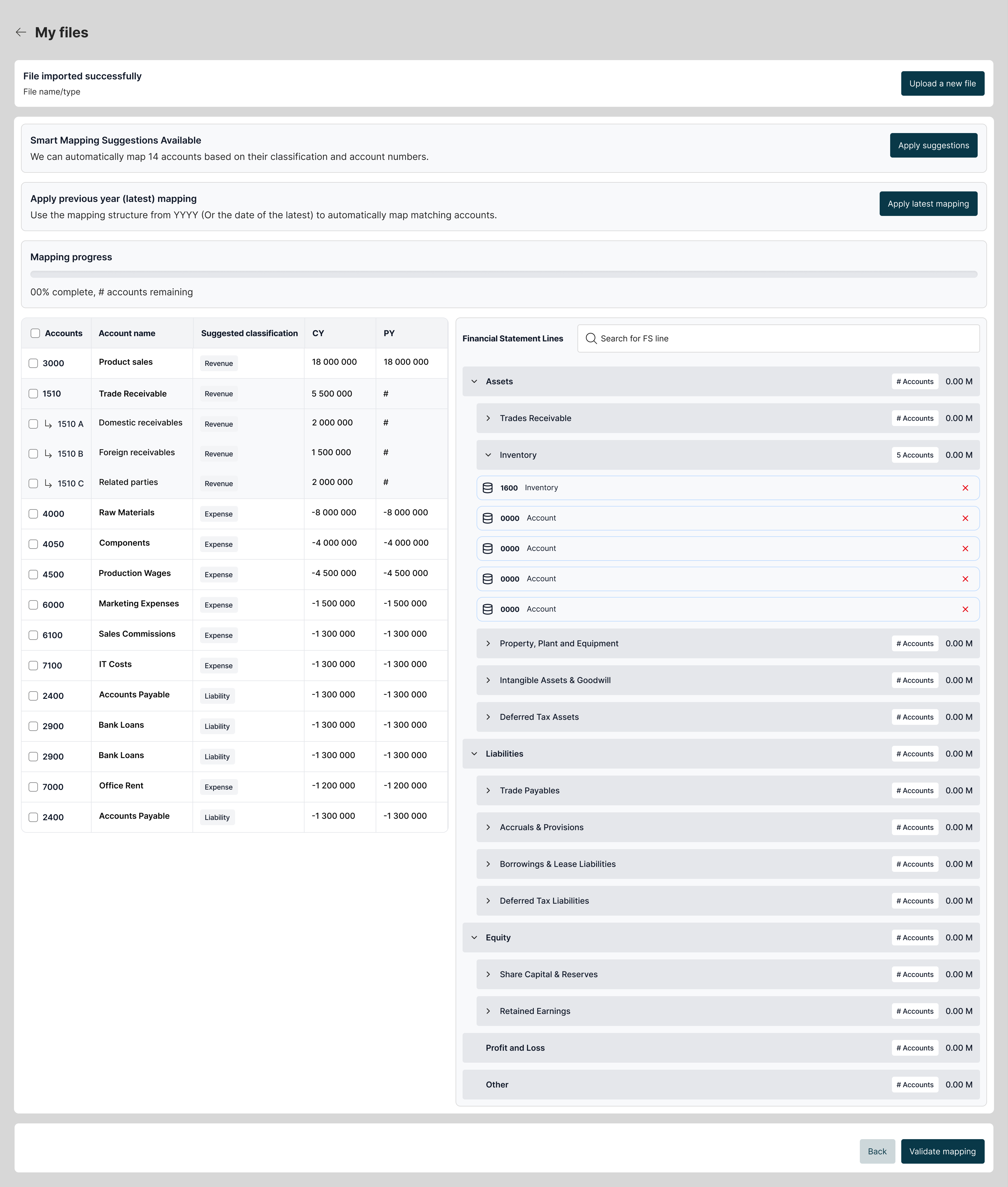

Financial data import and mapping interface — accounts are mapped to FS lines using smart suggestions or manually.

Risk assessment interface — FS line overview with the drill-in panel showing risk levels, assertions, and linked procedures.

Despite a tight timeline and a domain that required learning from scratch, the engagement moved faster than the client expected. Auditors who had been sceptical early on engaged actively by the later stages, and the client expressed genuine surprise at the pace and quality of progress given the complexity of what was being designed. The work established a solid UX foundation for a platform that had not previously existed in any structured form.

If I were starting this project again, I would push for domain immersion sessions with auditors even earlier, before any design work began. The time spent learning ISA standards independently was necessary, but some of the most valuable understanding came from conversations with the working group. Getting into those conversations sooner would have compressed the learning curve and given the design work a stronger foundation from the start.